Credit card transactions are processed through a variety of platforms, including brick-and-mortar stores, e-commerce stores, wireless terminals, and phone or mobile devices. The entire process — from the time you slide, tap or otherwise use your card until a receipt is produced — takes place within two to three seconds.

Although being familiar with the credit card transaction process may not seem useful to the average consumer, it provides valuable insight into the inner-workings of modern commerce as well as the prices we ultimately pay at the register. What’s more, knowledge of the credit card transaction process is extremely important for small business owners since payment processing represents one of the biggest costs that merchants must confront.

Credit Card Transaction Process

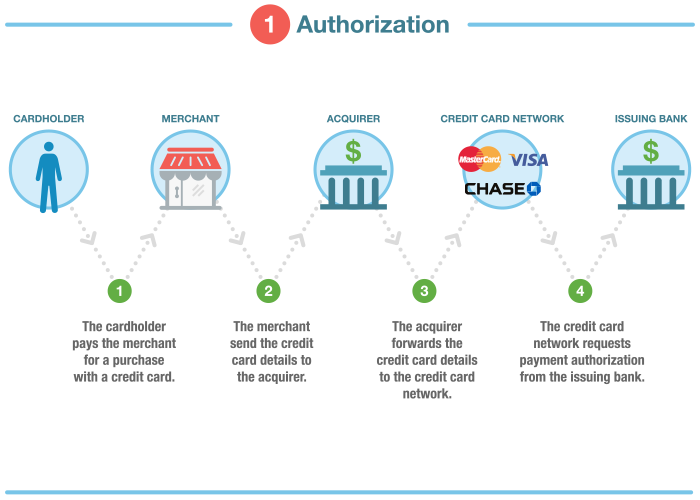

Stage 1: Authorization

In the authorization stage, the merchant must obtain approval for payment from the issuing bank.

- The cardholder presents their credit card for payment to the merchant at the point of sale.

- After swiping their credit card on a point of sale (POS) terminal, the customer’s credit card details are sent to the acquiring bank (or its acquiring processor) via an Internet connection or a phone line.

- The acquiring bank or processor forwards the credit card details to the credit card network.

- The credit card network clears the payment and requests payment authorization from the issuing bank. The authorization request includes the following:

- Credit card number

- Card expiration date

- Billing address — for Address Verification System (AVS) validation

- Card security code — CVV, for instance

- Payment amount

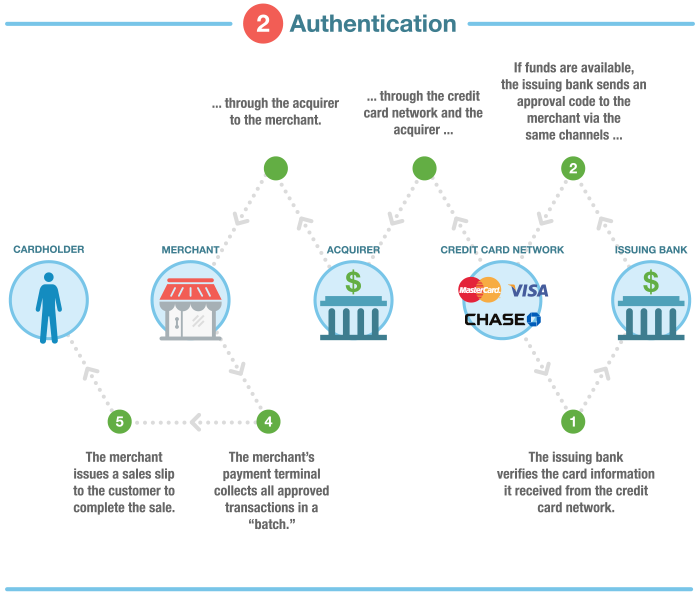

Stage 2: Authentication

In the authentication stage, the issuing bank verifies the validity of the customer’s credit card using fraud protection tools such as the Address Verification Service (AVS) and card security codes such as CVV, CVV2, CVC2 and CID.

- The issuing bank receives the payment authorization request from the credit card network.

- The issuing bank validates the credit card number, checks the amount of available funds, matches the billing address to the one on file and validates the CVV number.

- The issuing bank approves, or declines, the transaction and sends back the appropriate response to the merchant through the same channels: credit card network and acquiring bank or processor.

- Once the merchant receives the authorization, the issuing bank will place a hold in the amount of the purchase on the cardholder’s account. The merchant’s POS terminal will collect all approved authorizations to be processed in a “batch” at the end of the business day.

- The merchant provides the customer a receipt to complete the sale.

Stage 3: Clearing & Settlement

In the clearing stage, the transaction is posted to both the cardholder’s monthly credit card billing statement and the merchant’s statement. It occurs simultaneously with the settlement stage.

- At the end of each business day, the merchant sends the approved authorizations in a batch to the acquiring bank or processor.

- The acquiring processor routes the batched information to the credit card network for settlement.

- The credit card network forwards each approved transaction to the appropriate issuing bank.

- Usually within 24 to 48 hours of the transaction, the issuing bank will transfer the funds less an “interchange fee,” which it shares with the credit card network.

- The credit card network pays the acquiring bank and the acquiring processor their respective percentages from the remaining funds.

- The acquiring bank credits the merchant’s account for cardholder purchases, less a “merchant discount rate.”

- The issuing bank posts the transaction information to the cardholder’s account. The cardholder receives the statement and pays the bill.

Credit Card Transaction Participants

Before you can understand the process of a credit card transaction, it’s best first to familiarize yourself with the key players involved:

- Cardholder: While this is pretty self-explanatory, there are two types of cardholders: a “transactor” who repays the credit card balance in full and a “revolver” who repays only a portion of the balance while the rest accrues interest.

- Merchant: This is the store or vendor who sells goods or services to the cardholder. The merchant accepts credit card payments. It also sends card information to and requests payment authorization from the cardholder’s issuing bank.

- Acquiring Bank/Merchant’s Bank: The acquiring bank is responsible for receiving payment authorization requests from the merchant and sending them to the issuing bank through the appropriate channels. It then relays the issuing bank’s response to the merchant.

- Acquiring Processor/Service Provider: This third-party entity is sometimes an arm of the acquiring bank. A processor provides a service or device that allows merchants to accept credit cards as well as send credit card payment details to the credit card network. It then forwards the payment authorization back to the acquiring bank.

- Credit Card Network/Association Member: These entities operate the networks that process credit card payments worldwide and govern interchange fees. Examples of credit card networks are Visa, MasterCard, Discover and American Express. In the transaction process, a credit card network receives the credit card payment details from the acquiring processor. It forwards the payment authorization request to the issuing bank and sends the issuing bank’s response to the acquiring processor.

- Issuing Bank/Credit Card Issuer: This is the financial institution that issued the credit card involved in the transaction. It receives the payment authorization request from the credit card network and either approves or declines the transaction.

Credit Card Processing Fees & Costs

For the convenience of their customers, many merchants accept credit cards as payment. But you may have wondered why some merchants will accept only cash or require a minimum purchase amount before allowing the use of a credit card. Here’s why: Merchants must pay a price to accept credit card payments. Hence, most will seek the cheapest credit card processing rates or mark up the prices of their products so customers’ payments can absorb the card-processing cost.

Depending on the type of merchant and through which platform a good or service is delivered (e.g., at the retail store, through e-commerce or by phone), credit card processing rates will vary. They usually are charged as flat fees, per-transaction fees or volume-based fees. For the purpose of this guide, only major costs will be explained below:

Merchant Discount Rate: Merchants pay this fee for accepting credit card payments and receiving service from acquiring processors. It’s usually between 2% and 3% (online merchants pay the higher end) — to as much as 5% — of the total purchase price after sales tax is added. Also known as a discount fee, this rate comprises several components:

- Interchange Fee: The acquiring bank and acquiring processor pay this fee to the issuing bank. It is market-based and set by each credit card network (except American Express). Visa and MasterCard, for instance, update their interchange rates twice per year. Most interchange fees are assessed in two parts: a percentage to the issuing bank and a fixed transaction fee to the credit card network. For instance, the per-swipe fee might be 2.35% plus $0.15.Interchange fees vary and are categorized through a process called “interchange qualification,” which determines the rate based on several criteria:

- Physical presence or absence of the card during the transaction

- Processing method used (e.g., swiped, manually entered or e-commerce)

- Credit card company

- Card type (e.g., regular, premium, commercial, rewards or government-issued)

- Merchant’s business type (as determined by merchant category code)

- Assessments: Credit card networks (except American Express) charge this fee for transactions that are made with their branded cards. It usually is based on a percentage of the total transaction volume for the month. The fee usually is fixed, and the merchant’s acquiring bank may not charge a lower rate or negotiate a better deal with the merchant. Assessments generally are charged per transaction but can vary depending on the pricing model the merchant follows. For instance, Visa might charge a 0.11% assessment plus $0.0195 processing or usage fee for each card swipe. Assessment amounts may change periodically. Combined with the interchange fee, assessments constitute between 75% and 80% of total card-processing costs.

- Markups: Acquiring banks and acquiring processors usually will include a markup over interchange fees and assessments partly as profit and partly to cover the cost of facilitating credit card transactions. It constitutes between 20% and 25% of total card-processing costs. Merchants generally can negotiate the markup with the entities that charge them. Markups vary by processor and pricing model. They may also include other types of fees.

Chargebacks: Customers reserve the right to dispute a charge on their credit card billing statement within 60 days of the statement date. When the issuing bank receives a complaint from a customer, it charges the merchant between $10 and $50 as a penalty and for issuing a “retrieval request.” If the merchant doesn’t respond to the retrieval request within a certain timeframe, it could incur additional fees. The merchant may appeal, but the process is long and likely to favor the customer. If the merchant loses, the issuing bank will recover, or charge back, the customer’s payment.

When a Credit Card Transaction Gets Declined

Getting your credit card transaction declined is never enjoyable. It’s embarrassing. But the rejection of a credit card can be caused by other reasons besides maxing out the card.

When a credit card is declined, the point of sale (POS) terminal will return a response code that explains why. Sometimes those codes don’t tell the full story. In those instances, only your credit card issuer can identify the particular reason for the rejection, so you may need to call customer service to resolve the problem.

Below are some of the most common issues you might encounter if your card gets declined:

- Incorrect credit card number or expiration date

- Insufficient funds

- Some credit card companies reject international charges

- The issuing bank or credit card company experienced technical issues while your transaction was being processed

- If the customer made a large number of online purchases within a short period of time, some banks will reject several of the charges as a fraud-prevention measure

WalletHub experts are widely quoted. Contact our media team to schedule an interview.