The WalletHub.com Penalty APR Study evaluates the post-CARD Act Penalty APR policies of the top 10 credit card issuers, based on outstanding balances. The study only focused on the Penalty APR policies for existing transactions, as all credit card companies reserve the right to change the APRs for future transactions at any time. The study rated 4 of the 10 issuers as either Excellent or Good in the majority of categories for their Penalty APR policies. However, 6 of the 10 were rated poorly because they were either very vague or appeared to be utilizing the new rules to engage in “gotcha” rate practices. None of these six issuers clearly explain how the Penalty APR works and how it may affect consumers. This is not surprising, given that the study also found that the Sample Statement on the Federal Reserve’s Consumer’s Guide to Credit Cards does an equally poor job.

Below is a summary of the results:

When available, the study examined three different credit card applications from each issuer for clarity in the following categories: triggers for the Penalty APR, the portion of a balance affected by different triggers, the steps necessary to get back to the regular APR, and the disclosure of the law for the Penalty APR in the first year of a credit card agreement. The study evaluated the credit card applications themselves, and not Cardmember Agreements, as the terms and conditions on the applications are what consumers see before they apply for a credit card.

The study determined that the ideal statement would contain the following:

Trigger: The companies were rated on whether or not they clearly stated the Penalty APR trigger for being 60 days delinquent (the only trigger that affects existing transactions).

Portion of Balance Affected: The ideal disclosure clarifies which triggers affect what portion of a credit card balance. There are two types of triggers – one type affects new transactions, and the other can affect both new transactions and an existing balance. The only trigger that can affect an existing balance is a cardholder becoming 60 days or more delinquent in making a payment. All other triggers (e.g. making one late payment or going over the credit limit) can only affect new transactions. The companies were rated based on the extent to which they made it clear that being 60 days delinquent will affect your entire balance.

How to Get Back to Regular Rate: By law, making timely payments for 6 consecutive months will remove the Penalty APR from transactions made prior to the 14 days after a consumer got the notice of the rate increase (in simpler words, existing transactions). The companies were rated based on their disclosure of this information.

First Year Disclosure: The Credit CARD Act stipulates that the Penalty APR or any other rate increases cannot be applied to a credit card account in the first year that the account is open, unless the cardholder is 60 days delinquent. The companies were rated based on the clarity with which they disclosed this information.

BREAK DOWN BY ISSUER:

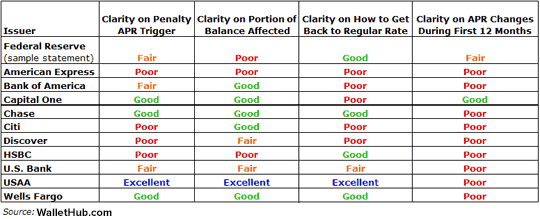

Federal Reserve (sample statement):

- Clarity on Penalty APR Trigger: FAIR - The Federal Reserve does not mention the trigger from being 60 days delinquent in the "Penalty APR and When it Applies" section. It is only mentioned later in an explanation of how to lose an introductory APR.

- Clarity on Portion of Balance Affected: POOR - The Sample Statement leaves out the fact that the triggers listed only apply to new transactions. Additionally, it does not clarify in "When it Applies" that if you are 60 days delinquent, the credit card company can apply the Penalty APR to your entire balance.

- Clarity on How to Get Back to Regular Rate: GOOD - The Federal Reserve clearly clearly states that the Penalty APR will be removed once you make the next 6 consecutive minimum payments.

- Clarity on APR Changes During First 12 Months: FAIR - The Federal Reserve mentions in the section on introductory rates that you cannot lose your intro rate in the first year unless you are 60 days delinquent. However, this is misleading because the way it is written implies that this rule only applies to the introductory rate, when in fact the Penalty APR cannot be applied to your account in any way during the first year unless you are 60 days delinquent.

American Express:

- Clarity on Penalty APR Trigger: POOR - American Express does not mention the 60 day delinquency trigger.

- Clarity on Portion of Balance Affected: POOR - American Express does not state that the triggers they mention can only affect future transactions - it does not mention that being 60 days delinquent is the only way it can apply the Penalty APR to the purchases made prior to the rate increase.

- Clarity on How to Get Back to Regular Rate: POOR - American Express leaves out that by law it is required to remove the Penalty APR from purchases made before the Penalty APR took effect after you've made the minimum payment for 6 consecutive months.

- Clarity on APR Changes During First 12 Months: POOR - American Express states that it may change any terms for existing and future balances at any time, subject to applicable law. This is misleading because in the first year, it cannot reprice any of your APRs unless you are 60 days delinquent.

Bank of America:

- Clarity on Penalty APR Trigger: FAIR - Bank of America states that it will reprice your APR if you are 60 days delinquent, however it does not mention a specific Penalty APR and does not refer to it as a Penalty APR. It also does not put this condition in the APR section of the agreement.

- Clarity on Portion of Balance Affected: GOOD - Bank of America specifies that being 60 days delinquent gives it the right to change all interest rates, including existing promotional rate balances.

- Clarity on How to Get Back to Regular Rate: POOR - Bank of America leaves out that by law it is required to remove the Penalty APR from purchases made before the Penalty APR took effect after you've made the minimum payment for 6 consecutive months.

- Clarity on APR Changes During First 12 Months: POOR - Bank of America states that the APRs in your agreement are subject to change. This is misleading because in the first year, it cannot reprice any of your APRs unless you are 60 days delinquent.

Capital One:

- Clarity on Penalty APR Trigger: GOOD - Capital One says it can apply the Penalty APR if you are 60 days delinquent.

- Clarity on Portion of Balance Affected: GOOD - Capital One states that if you are 60 days delinquent that the Penalty APR will apply to both existing and future transactions, and other APR increases will only apply to new transactions.

- Clarity on How to Get Back to Regular Rate: POOR - Capital One leaves out that by law it is required to remove the Penalty APR from purchases made before the Penalty APR took effect after you've made the minimum payment for 6 consecutive months.

- Clarity on APR Changes During First 12 Months: GOOD - Capital One clearly states that your interest rate will not be affected for the first year of your account unless you are 60 days delinquent.

Chase:

- Clarity on Penalty APR Trigger: GOOD - Chase clearly states that making a late/returned payment or exceeding your credit limit will trigger the Penalty APR for new transactions - and that if you are 60 days delinquent it will apply to your whole balance.

- Clarity on Portion of Balance Affected: GOOD - Chase specifies that the triggers listed only apply to new transactions, unless you are 60 days delinquent.

- Clarity on How to Get Back to Regular Rate: GOOD - Chase specifies that 6 consecutive months of timely payments will get you back to your regular rate for purchases made prior to the 14 days after you received notice.

- Clarity on APR Changes During First 12 Months: POOR - Chase states that the APRs in your agreement are subject to change. This is misleading because in the first year, it cannot reprice any of your APRs unless you are 60 days delinquent.

Citi:

- Clarity on Penalty APR Trigger: POOR - Citi does not mention the 60 day delinquency trigger.

- Clarity on Portion of Balance Affected: POOR - Citi does not state that the triggers they mention can only affect future transactions - it does not mention that being 60 days delinquent is the only way it can apply the Penalty APR to purchases made before you received notice of the rate increase.

- Clarity on How to Get Back to Regular Rate: GOOD - Citi clearly states that the Penalty APR will no longer apply to existing balances after you make 6 consecutive payments on time.

- Clarity on APR Changes During First 12 Months: POOR - Citi states that you may lose your introductory APR and get the Penalty APR if you make a late payment. This is misleading because in the first year, it cannot reprice any of your APRs unless you are 60 days delinquent.

Discover:

- Clarity on Penalty APR Trigger: POOR - Discover does not mention the 60 day delinquency trigger.

- Clarity on Portion of Balance Affected: FAIR - Discover makes the distinction between new and existing transactions, however it fails to mention that only the 60 day delinquency trigger can affect transactions that happened before you received notice of the rate increase.

- Clarity on How to Get Back to Regular Rate: POOR - Discover leaves out that by law it is required to remove the Penalty APR from purchases made before the Penalty APR took effect after you've made the minimum payment for 6 consecutive months.

- Clarity on APR Changes During First 12 Months: POOR - Discover mentions that the APRs in your agreement are subject to change to the extent permitted by law. This is very vague and does not let you know that in the first year, it cannot reprice any of your APRs unless you are 60 days delinquent.

HSBC:

- Clarity on Penalty APR Trigger: POOR - HSBC does not mention the 60 day delinquency trigger.

- Clarity on Portion of Balance Affected: POOR - HSBC does not clarify that missing one payment will only affect future transactions. It does not mention that being 60 days delinquent is the only way it can apply the Penalty APR to purchases made before you received notice of the rate increase.

- Clarity on How to Get Back to Regular Rate: GOOD - HSBC clearly states that the Penalty APR will be removed once you make the next 6 consecutive minimum payments.

- Clarity on APR Changes During First 12 Months: POOR - HSBC mentions that the APRs in your agreement are subject to change. This is misleading because in the first year, it cannot reprice any of your APRs unless you are 60 days delinquent.

U.S. Bank:

- Clarity on Penalty APR Trigger: FAIR - U.S. Bank does not mention a Penalty APR, which most likely means that it does not use one for existing transactions. Had they explicitly stated that it does not use a Penalty APR, it would have received an Excellent rating in this category.

- Clarity on Portion of Balance Affected: FAIR - U.S. Bank does not mention a Penalty APR, which most likely means that it does not use one for existing transactions. Had they explicitly stated that it does not use a Penalty APR, it would have received an Excellent rating in this category.

- Clarity on How to Get Back to Regular Rate: FAIR - U.S. Bank does not mention a Penalty APR, which most likely means that it does not use one for existing transactions. Had they explicitly stated that it does not use a Penalty APR, it would have received an Excellent rating in this category.

- Clarity on APR Changes During First 12 Months: POOR - U.S. Bank mentions that the APRs in your agreement are subject to change. This is misleading because in the first year, it cannot reprice any of your APRs unless you are 60 days delinquent.

USAA:

- Clarity on Penalty APR Trigger: EXCELLENT - Based on the credit card applications we examined, USAA does not apply a Penalty APR to its credit card accounts.

- Clarity on Portion of Balance Affected: EXCELLENT - For existing balances, USAA clearly states that it does not use a Penalty APR.

- Clarity on How to Get Back to Regular Rate: EXCELLENT - USAA does not need instructions on how to get back to the regular rates for exisiting transactions because it clearly states that it does not apply a Penalty APR for those transactions.

- Clarity on APR Changes During First 12 Months: POOR - USAA mentions that the APRs in your agreement are subject to change. This is misleading because in the first year, it cannot reprice any of your APRs unless you are 60 days delinquent.

Wells Fargo:

- Clarity on Penalty APR Trigger: GOOD - Wells Fargo clearly states that being 60 days delinquent will result in the Penalty APR on your account.

- Clarity on Portion of Balance Affected: GOOD - Wells Fargo says that the Penalty APR will apply to all balances if you are 60 days delinquent.

- Clarity on How to Get Back to Regular Rate: GOOD - Wells Fargo clearly states that the Penalty APR for being 60 days delinquent will no longer apply to your account after you make 6 consecutive payments on time.

- Clarity on APR Changes During First 12 Months: POOR - Wells Fargo mentions that the APRs in your agreement are subject to change. This is misleading because in the first year, it cannot reprice any of your APRs unless you are 60 days delinquent.

For questions or more information regarding this study, please contact our media department.

WalletHub experts are widely quoted. Contact our media team to schedule an interview.