We can’t tell you what happens when you die, but we can tell you what will happen to your debt. Whether you owe money on credit cards, mortgages, student loans or other types of debt, the rule of thumb is that your heirs will not be held liable. In other words, individuals cannot “pass on” or “inherit” debt when a loved one passes away.

There are, however, a few important exceptions to this rule. To learn more, continue reading below.

Debt Liability and Exceptions

When an individual incurs debt, that person tends to be the only one legally liable for it. Their own assets – collectively known as their “estate” – will be used to pay off creditors upon death. If the debts exceed the estate’s value, they’re simply written off as a loss by lenders. Such debt essentially dies with the deceased.

Having said that, there are certain exceptions to this rule, which depend on the deceased’s location, type of debt and whether or not a third-party was involved.

- Community Property States – Creditors may hold a surviving spouse responsible for repayment of debts incurred during marriage in a community property state.

- Vested Third Parties – Lenders can hold co-signers and guarantors liable for debts when the main borrower passes away. Note that authorized users on credit cards are exempt from liability, as they simply benefit from using another person’s account and are not responsible for payments.

- Student Loans – In most cases, no one is held liable – not even the decedent’s estate – for federal student loans. They’re completely discharged upon death. Unfortunately, few private student loans get the same treatment.

- Mortgages – Federal law allows one’s surviving spouse to assume a loan’s liability if he or she wishes – so as to continue living in the home. The spouse must simply prove capable of continuing mortgage payments.

- Loans Bequeathed in a Will – Debt liability can technically be passed down via a will if it’s attached to an asset that has not been sold off during the probate process. Don’t worry – this can only occur if the asset’s value outweighs the debt owned on it (so really, it’s more of an asset than a debt).For example, if a decedent bequeathed his car to his daughter, she can gain possession of the car along with the responsibility for paying off the remaining auto loan balance.

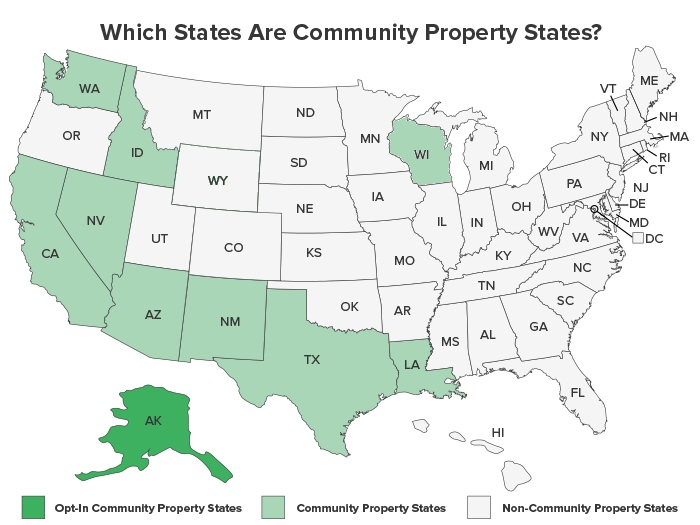

Community Property States:

Community Property States consider any debt or property acquired during a marriage to be “communal,” rendering both parties legally responsible for them. So, if your spouse racked up a massive credit card bill while you were married and then passed away, you would be responsible for repayment – even if the account was only in your spouse’s name.

The following graph illustrates which states do and do not employ community property rules. Alaska, as you’ll see, is an opt-in community property state – allowing you to choose the communal policy if you wish.

How Debt Gets Paid Off: The Probate Process

We’ve now established that debts incurred in community property states as well as those involving co-signers or guarantors may be passed down to loved ones upon the borrower’s demise. But what about debts that are the sole responsibility of the deceased?

Whether or not the decedent died “intestate” (meaning they didn’t have a valid will), such debts are repaid using the deceased’s assets during what’s known as the “probate process.”

The executor (aka. “administrator”) – who is typically appointed on the will, if there is one – is responsible for liquidating the estate’s assets to satisfy obligations to lenders. In the event there is no will or appointed executor, another individual will be selected to meet the duties according to a legal proceeding. Depending on which state you reside in, that person could be the spouse, children, parents, etc.

This, of course, begs the question: Which assets are fair game for probate and which are off limits? For starters, only assets filed solely under the deceased person’s name can be used, meaning shared assets are safe.

To better understand which assets can and cannot be liquidated, see the table below:

| Examples of Probate Property | Examples of Non-Probate Property |

|---|---|

|

|

Once the necessary funds have been raised from the probate process, amounts are distributed in a particular order. In fact, creditors aren’t necessarily paid off first.

Payouts are typically made in the following order:

| Administrative Costs | This typically includes funeral expenses and probate charges (e.g. attorney and court filing fees). |

| Family Allowances | If there is a surviving spouse or any children under the age of 18, they will each receive an allowance large enough to support them for about a year (exact amounts vary across states). |

| Creditors | In some states, creditors are prioritized equally, meaning that all debts are paid off in equal percentages until there is a shortage of funds.

Other states have priority lists, which ensure that certain creditors receive payment before others. |

| Heirs | Any remaining assets – including those left in the will – are distributed amongst one’s heirs. |

Helpful Tips To Consider

Coping with a loved one’s death is hard enough without having to worry about sorting out their debts. Here are some useful tips that will make the process as easy as possible:

- Know Your Rights with Debt Collectors – Debt collectors aren’t allowed to contact you for repayment unless youre legally liable for a relative’s debt. Nevertheless, there have been numerous reports of debt collectors harassing relatives of the deceased without legal grounds.If this ever happens to you, you can file a complaint with the Consumer Financial Protection Bureau.

- Protect Your Heirs – To secure assets for your heirs (and ensure they’re not sold off during the probate process), make sure to designate them as beneficiaries on any retirement/brokerage/bank accounts, life insurance policies, etc. Such accounts would then not be subject to the probate process.Merely listing your heirs as the recipients of valuables in your will is not enough, as those items are not off-limits to the probate process.

- Shield Yourself From Unnecessary Liability – Be extremely wary of being someone’s guarantor or co-signer. As outlined above, you will be held responsible for their debts if they pass away before paying it. You should therefore explore all possible alternatives.For example, if you’re managing the finances of your elderly parents, consider getting a power of attorney rather than co-signing for a loan or credit card. This gives you authority and convenient access to sorting their affairs, without being held responsible for their debts.

- Keep Each Other In Check – If you’re married and live in a community property state, make sure to keep your spouse’s spending in check. After all, you don’t want to be left with a pile of their debt when they pass on.

WalletHub experts are widely quoted. Contact our media team to schedule an interview.