American Express’s Late Payment Policy is Out of Sync with Industry

WalletHub.com decided to investigate the late payment policies of major credit card issuers after an experience that our CEO had with American Express. He recently realized he was 12 days past due in making a payment for his American Express credit card bill. When he went to pay his bill online, he received a message informing him that he was 30+ days past due. We were surprised by this, as it is counterintuitive, and decided to investigate the past-due policies of the six largest credit card issuers (based on outstanding balances).

We reached out to the spokespeople for each credit card issuer in the group, using the following example to better understand their late policies:

- Customer A has a credit card bill that was generated on August 2nd and payment is due on August 27th. If Customer A does not make their credit card payment until September 3rd (seven days past the due date, and 1 day after the next bill was generated), how many days past due is Customer A considered?

In addition to asking about the late payment policies, we also asked the issuers when they report delinquencies to the credit bureaus, as these two policies have a significant impact on one another. Below you will find a summary table of the results:

| Issuer | Number of Days Past Due (based on above example) |

When Issuer Reports to Credit Bureaus |

| American Express | 30+ | Varies |

| Bank of America | 7 | 30 days past due |

| Capital One | 7 | 30 days past due |

| Chase | 7 | 30 days past due |

| Citi | 7 | 65 days past due |

| Discover | 7 | 30 days past due |

(Source: WalletHub.com)

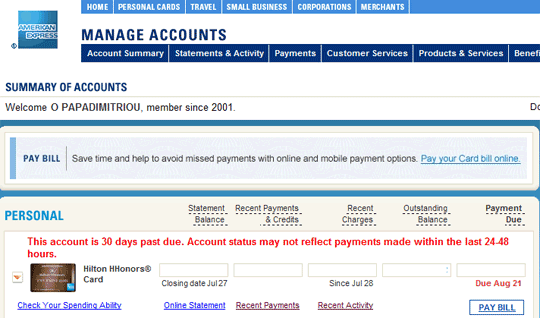

Our understanding was that Customer A should be considered 7 days past due on September 3rd. The study found that this was the case for all of the issuers (including Bank of America, Chase, Discover, Capital One, and Citi), except American Express. A member of the Executive Consumer Relations team confirmed that, “A person will be considered 30+ days past due on both charge card and credit card accounts if they have not made a payment by the time the next bill is generated” (September 2nd in the example above). This confirmation, in addition to a phone call to a customer service representative and a screen shot of our CEO’s past due account, verifies that American Express is the only issuer to use the aggressive and counterintuitive late payment policy that we were initially surprised by.

Implications:

- American Express is out sync with the rest of the industry. The last thing that consumers need right now is an open door for each credit card company to come up with their own method for determining their customers’ late status. The new credit card law (Credit CARD Act) was meant to bring clarity and uniformity to an industry that was lacking both, and practices like this undermine these efforts.

- American Express customers who have missed their payment due date by a few days are being told that they are 30+ days past due, when in reality they are not. The incorrect message that American Express is communicating to their customers may be stressful for those who know that most credit card companies will report them to the credit bureaus once they become 30+ days delinquent.

In addition to these indisputable implications, an aggressive late payment policy such as the one used by American Express also raises questions about when American Express applies the penalty APR to its customers’ accounts and whether or not it inflates its customers’ delinquency status when reporting to the credit bureaus. Both of these things depend on how many days past due a person is in making a payment, and since American Express prematurely counts its customers as being 30+ days past due, it also makes sense that they might prematurely apply the penalty APR and incorrectly report delinquency status.

In order to get answers to these questions, we made a phone call to a customer service representative, contacted a member of their Executive Consumer Relations team, and contacted a spokeswoman from American Express’s Public Relations team to ask about their penalty APR and delinquency policies. We got conflicting answers on both accounts.

In regards to the penalty APR, the representatives in customer relations (including the representative from the executive team) confirmed that American Express is in fact prematurely applying the penalty APR to their customers’ accounts. The Credit CARD Act states that the regular APR for an existing balance cannot be increased unless a consumer is a full 60 days past due. However, due to the way American Express counts the days past due, a customer is considered 60+ days past due when they are really only 30+ days past due. Both customer service representatives confirmed that the penalty APR would be applied to a customer’s account when they are 60 days past due based on American Express’s definition of past due (missing only 2 payments).

However, the PR spokeswoman said that American Express does not prematurely increase the APRs on their customers’ accounts and that a customer must miss 3 payment deadlines (60 days past the first payment deadline) before the penalty APR will be applied to a customer’s account. She said the confusion was due to the fact that “American Express has a different nomenclature for its aging than other issuers,” but its practice is the same. According to the spokeswoman, 30 days past due at American Express means that the bill is 30 days ‘aged’, which is counted from the time the bill is generated and not the date the bill is due.

The issue is similar in regards to reporting delinquency status. Both members from the customer relations team confirmed that when a customer is 120 days past due, based on American Express's definition, that customer is reported to the credit bureaus as being 120 days delinquent. This means that a customer would be reported to the credit bureaus as being 120+ days delinquent when they are really only 90+ days delinquent. The PR spokeswoman, however, said that American Express does not even report the number of days a customer is delinquent to the credit bureaus and instead only reports whether a customer is in collections or not.

Due to the seriousness of these implications, we are inclined to believe that the PR spokeswoman is correct and American Express is not in fact prematurely increasing its customers’ APRs and incorrectly reporting delinquencies to the credit bureaus. However, the fact remains that they are prematurely classifying their customers as being 30+ days past due. Although they say this is a nomenclature issue, the phrase ‘past due’ is not an ambiguous term. ‘Past due’ means past the due date for payment, not past the time a bill was generated.

At a minimum, this bizarre ‘nomenclature’ has both American Express customers and its own customer relations team confused. It is obvious that American Express needs to sort this out internally, but it is even more important that they relay the correct message to their customers. Customers are currently being told that they are 25 days more past due than they actually are, a practice that is not only inaccurate, but also inconsistent with the rest of the credit industry.

Exhibit A: Screenshot of WalletHub.com’s CEO’s 30+ days past due message

For questions or more information regarding this study, please contact our media department.

WalletHub experts are widely quoted. Contact our media team to schedule an interview.