Merchant category codes, or MCC’s, are often overlooked – in fact, not many consumers even know they exist. Essentially, merchant category codes are 4-digit numbers that credit card networks – such as VISA, MasterCard, American Express and Discover – assign to businesses in order to classify them into certain industries. Because these codes are based upon the types of goods and/or services a merchant provides, they can range from industries as broad as “groceries” and “fuel” to those as specific as “wig and toupee stores.”

Though MCC’s were originally created by card networks to assist the IRS in tax reporting, they have since been used for other purposes, such as assisting the networks in determining interchange fees (as networks charge less in certain industries than others). However, from a consumer’s perspective, merchant category codes are most important as they pertain to credit card rewards. Many credit cards provide different rewards earning rates for purchases made in different spending categories – such as gas, groceries or dining – which makes the way a given merchant is classified very important. For instance, if you have a credit card that offers extra rewards on purchases made at grocery stores but your local Walmart is classified as a department store, you won’t be earning the bonus perks you might assume you’re getting.

For more information about how you can use merchant category codes to maximize your rewards earnings, where you can locate them and more, read on below.

Using Merchant Category Codes to Maximize Rewards

Though using merchant category codes is conducive to maximizing rewards on credit cards that offer higher earning rates in particular spending categories, it can be tricky chiefly due to three main reasons.

First, MCC’s are assigned on a store-basis rather than on an item-basis – this places the emphasis on where you buy your item, not what item you buy. Many consumers fail to realize this, leading them to believe they received extra points when they didn’t. For example, if your credit card offers 3X the points in the dining category, your purchase needs to be from a store coded under one of the industries associated with ‘dining’ in order for you to receive those extra points. However, if the store is coded under a different industry – a deli being classified as a convenience store, for instance, your transaction won’t count towards dining even if you did have lunch.

Merchant category codes can cause further confusion among consumers due to the fact that each credit card network may assign a different industry code to the same retailer (though this is rarely the case). For example, MasterCard might classify John’s Convenience Store under “Eating Places, Restaurants” while VISA might classify it under “Miscellaneous Food Stores - Convenience Stores and Specialty Markets”.

Lastly, just to complicate things a little more, not all branches of the same retailer are given the same merchant code – a K-Mart may be classified under “Discount Stores” in one area but under “Department Stores” in another. This is because credit card networks code a store’s industry depending on its primary line of business, which can vary between branches.

These variations make it necessary to check the merchant category code for each individual store that you patron if you truly want to maximize the value of a credit card with category-based bonus rates. The need to do so is even more pronounced when it comes to credit cards whose bonus categories change periodically. We at WalletHub advise you to select cards with stable bonus categories versus rotating ones for several reasons.

First, rotating categories change on a quarterly basis, which means you’d have to constantly check which industries are eligible and therefore what stores you can shop at, and then adjust your spending habits accordingly in order to maximize your earnings. That’s just not feasible for most people. Furthermore, rotating categories often provide bonuses on low-dollar-amount purchases that you make relatively infrequently – such as “movies.” You can only rack up so much rewards value in such categories. Finally, most credit cards issuers mandate that you have to sign-up for the category in order to earn in it, and since many people are unaware of this or often forget to do so, they lose out on numerous points.

Where are Merchant Category Codes Listed?

The first way to determine a retailer’s merchant category code is to simply check how a purchase at that store appears on your credit card statement. This information will be displayed in one of three ways.

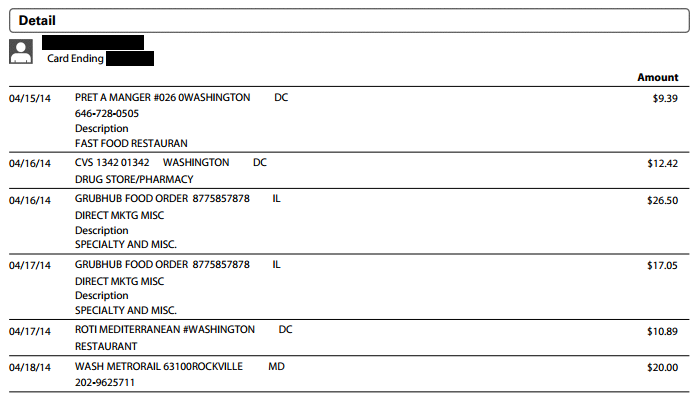

Some issuers simply state what industry a given transaction is classified under (and don’t be alarmed if a given merchant is classified as being in multiple industries – this can happen). For example, take a look at this online statement from American Express’s Blue Cash Preferred Card. The industry is listed under each merchant name:

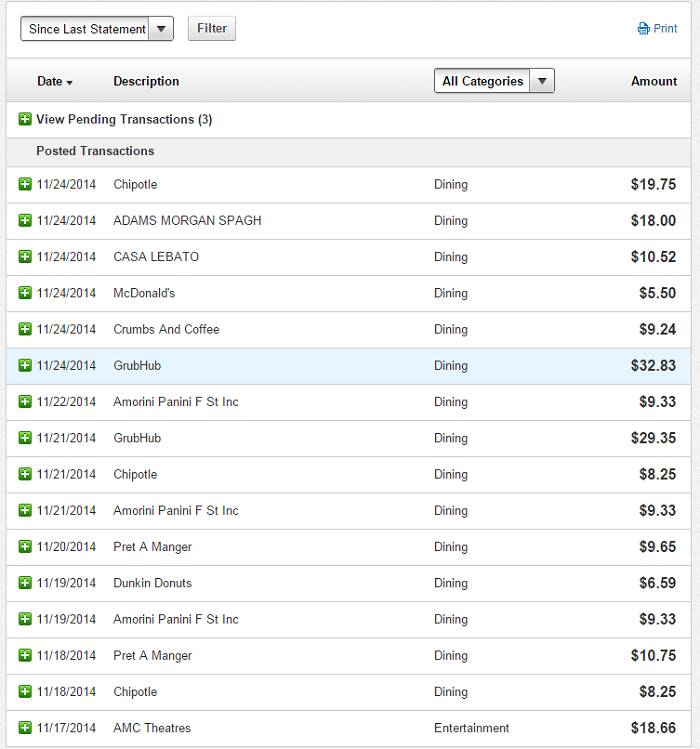

Alternatively, other issuers will cut right to the chase and list the spending category your purchase falls in rather than the industry it pertains to. For example, consider how “GrubHub” is classified as being in the “Dining” category in the Capital One statement below, versus being mapped to the “Specialty and Misc.” industry in the above Amex statement:

Finally, other issuers will only include the 4-digit merchant category code itself, leaving one to guess what industry the business actually belongs in. In events like this, you’ll need to consult a code table to see what industry title your numerical code correlates to. Note that all credit card networks utilize the same code table as they systematically use the same numbers to refer to the same industries.

In order to save you some time, we’ve listed the most common merchant category codes in the table below. These are also the codes that are most frequently associated with credit card bonus categories:

| Merchant Category Code | Industry |

|---|---|

| 5812 | Eating Places, Restaurants |

| 5912 | Drug Stores and Pharmacies |

| 5814 | Fast Food Restaurants |

| 5941 | Sporting Goods Stores |

| 5661 | Shoe Stores |

| 5691 | Men’s, Women’s Clothing Stores |

| 5712 | Furniture, Home Furnishings, and Equipment Stores, Except Appliances |

| 5732 | Electronics Stores |

| 5942 | Book Stores |

| 5943 | Stationery Stores, Office, and School Supply Stores |

| 5813 | Drinking Places |

| 5542 | Automated Fuel Dispensers |

| 5411 | Grocery Stores, Supermarkets |

| 5311 | Department Stores |

| 5310 | Discount Stores |

| 4121 | Taxicabs/Limousines |

| 4131 | Bus Lines |

| 4789 | Transportation Services |

| 4511 | Airlines, Air Carriers |

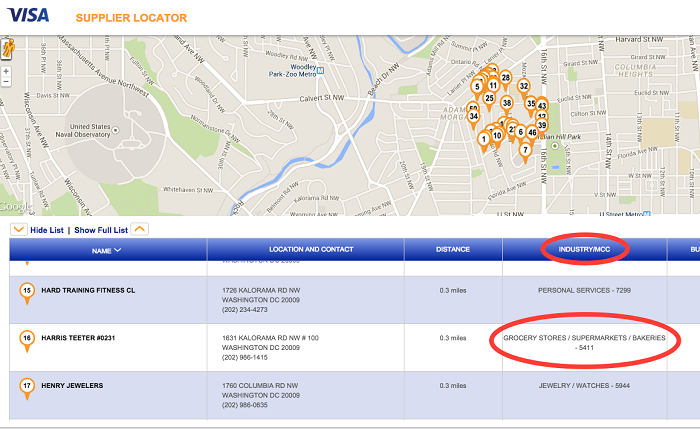

Now, if you are trying to acquire the merchant category code of a store that you have yet to make a purchase at, you can always use the VISA supplier tool. Even if your credit card doesn’t belong to VISA, you can still use this tool to extrapolate the information to your network. As mentioned previously, it is generally rare that credit card networks code the same businesses in different ways. If VISA codes a merchant under a particular industry, then it’s very likely that the other networks have done the same.

In order to determine a store’s MCC using the tool, simply enter the store’s address into the tool and select the correct result – it should look something like this:

What Are Transaction Category Codes?

MasterCard uses transaction category codes, also known as TCC’s, in addition to merchant category codes. A transaction category code is a single letter that is listed at the end of a 4-digit merchant category code on your statement, indicating the general industry that a merchant belongs to. The MCC then provides the specifics. For example, the TCC letter would indicate “Restaurant” while the MCC digits would indicate “Fast Food Restaurant”.

The TCC can therefore be used as a shortcut – at times, examining the letter alone is enough to determine whether a store transaction can count towards any particular bonus categories. For example, if the letter X is displayed as a part of the code for a purchase on your statement (X codes for “Airline /Railroad/Travel Agency/Transportation”), then you can safely assume – without looking up the 4-digit number – that the transaction counted towards your travel bonus category.

MasterCard’s transaction category codes are listed below:

| TTC | General Industry |

|---|---|

| A | Automobile/Vehicle Rental |

| C/Z | Cash Disbursement |

| F | Restaurant |

| H | Hotel/Motel |

| O | College/School Expense/Hospital |

| P | Payment Service Provider |

| R | All Other Merchants/U.S. Post Exchange/Cardholder-Activated Terminal |

| T | Pre-Authorized Mail/Telephone Order |

| U | Unique Transaction Quasi-Cash Disbursement/Cardholder-Activated Terminal |

| X | Airline/Railroad/Travel Agency/Transportation |

What’s the Difference Between MCC’s and NAICS Codes?

You might have heard of NAICS codes before, and we know that these acronyms can get a little confusing. Essentially, Merchant Category Codes (MCC) and North American Industry Classification System codes (NAICS) are independent sets of systems that happen to complete the same function – they both classify businesses into particular industries. However, NAICS codes were created by the U.S. government for economic data-gathering purposes, while merchant category codes were created by credit card networks primarily for tax reporting purposes. Regardless, the main distinguishing factor now is that credit card issuers rely on MCC’s – and not NAICS codes – to determine whether a purchase qualifies under a rewards bonus category or not.

WalletHub experts are widely quoted. Contact our media team to schedule an interview.